Let’s be honest: when most of us first moved into our own place, renters insurance was probably the last thing on our minds. Between figuring out how to split utility bills and hunting for the perfect couch, protecting our belongings felt like a “future problem.” But here’s the thing — it’s one of the smartest financial moves any renter can make, and once we discovered Lemonade, signing up became surprisingly easy.

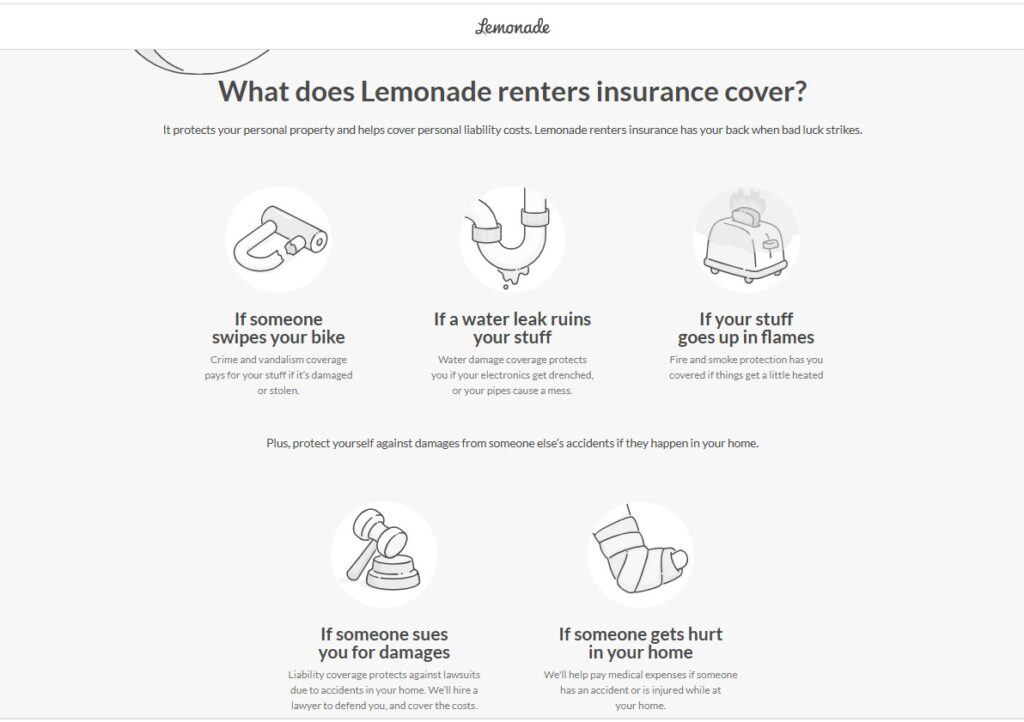

Renters insurance in the United States is a type of policy designed to protect tenants from the financial fallout of life’s unexpected moments. It typically covers personal belongings against theft, fire, vandalism, and certain types of water damage. It also provides liability coverage if someone gets injured in our home and can help pay for temporary living arrangements if our apartment becomes unlivable due to a covered loss. Yet, despite how essential it is, millions of renters in the U.S. still go without it.

That’s exactly where Lemonade comes in. Built from the ground up as a digital-first insurance company, Lemonade is rewriting the rulebook on what renters insurance can and should look like. With plans starting at just USD 5 per month, it’s accessible, fast, and refreshingly transparent. For Gen Z and Millennials who’ve grown up expecting things to work instantly and intuitively, Lemonade isn’t just another insurance option — it’s the only one that truly speaks our language.

Transparent, Honest Pricing With No Hidden Conflicts of Interest

10

One of the most persistent frustrations with traditional insurance is the feeling that the company is always looking for a reason not to pay our claim. That suspicion isn’t unfounded — conventional insurers profit from whatever premium money is left over after claims and expenses, which can create a financial incentive to minimize payouts.

Lemonade was explicitly designed to eliminate that conflict. The company takes a flat fee from our premium to cover operating costs, and everything else goes into a pool used to pay claims. Leftover money that isn’t used for claims doesn’t go to shareholders — it goes to the Giveback program. This means Lemonade has no financial incentive to deny our legitimate claims. Our interests and Lemonade’s interests are aligned from day one. That kind of radical transparency resonates deeply with a generation that grew up watching corporations get caught out for prioritizing profits over people. With Lemonade, we genuinely believe the system is set up to work for us — not against us.

See on:

The Giveback Program: Insurance That Aligns With Our Values

9

Here’s something no traditional insurance company has ever offered: a built-in charitable giving mechanism baked directly into the business model. When we sign up with Lemonade, we choose a cause we care about — whether that’s environmental protection, education, animal welfare, or social justice — and Lemonade directs a portion of unclaimed premiums to nonprofits supporting those causes through its annual Giveback program.

In 2025, this initiative resulted in more than USD 2 million in donations to causes chosen by Lemonade’s customers. For Millennials and Gen Z who consistently prioritize social responsibility when choosing brands, this is huge. We don’t want to just buy insurance — we want our money to mean something. Lemonade is a certified B-Corp and Public Benefit Corporation, meaning that doing good is legally embedded in its mission, not just a marketing talking point. No other major renters insurance provider offers anything remotely close to this kind of values-driven model.

See on:

A Top-Rated App That Makes Managing Insurance Feel Effortless

8

Lemonade’s app holds a near-perfect rating on both the App Store and Google Play, and it earns every bit of that praise. Every single aspect of our insurance relationship with Lemonade lives inside the app: purchasing a policy, updating coverage limits, filing a claim, adding a roommate or partner to our policy, and canceling if we move. There’s no need to call a 1-800 number or wait for a paper statement in the mail.

For a generation that manages everything from banking to healthcare on our phones, this is exactly what we expect. But Lemonade doesn’t just meet that expectation — it exceeds it. The interface is clean, intuitive, and genuinely pleasant to use (which is not something many of us have ever said about an insurance app). The experience of interacting with Lemonade’s platform feels more like using a well-designed consumer app than dealing with an insurance company, because at its core, that’s exactly what it is.

See on:

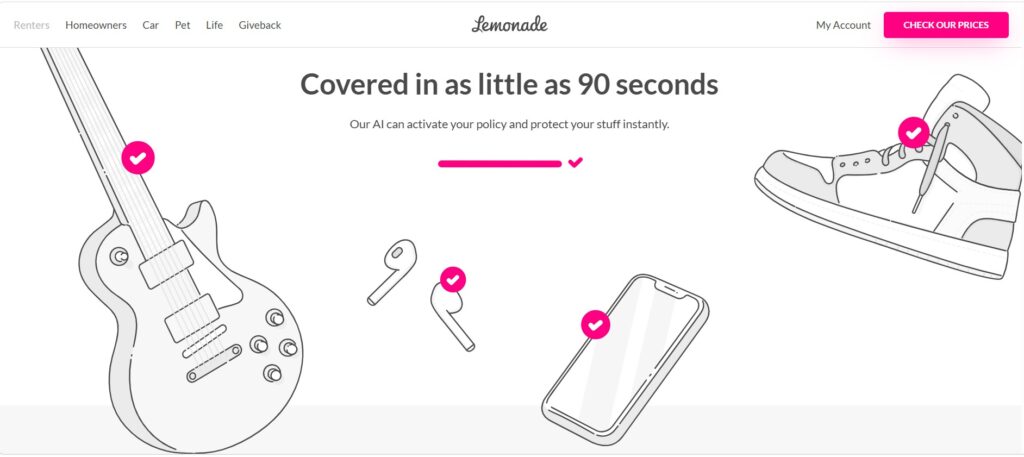

Extra Coverage Add-Ons for High-Value Items We Actually Own

7

Standard renters insurance policies have sub-limits for categories like electronics, jewelry, musical instruments, and bicycles. In plain terms: if our USD 2,500 laptop or USD 1,800 camera gets stolen, a basic policy might only reimburse a fraction of its value. Lemonade offers optional add-ons — also called scheduled personal property endorsements or “Extra Coverage” — that let us insure specific high-value items for their full replacement cost.

This is a game-changer for our generation. We own more valuable technology, gear, and collectibles than any renter demographic before us. Vintage guitars, professional camera equipment, high-end gaming setups, luxury streetwear — these are real assets that deserve real protection. Adding scheduled coverage for specific items through the Lemonade app takes about 60 seconds, and we can do it at any time without waiting for an annual renewal. That kind of on-demand flexibility is something traditional insurers, with their rigid annual policy structures, simply aren’t designed to offer.

See on:

Loss of Use Coverage for When Home Becomes Unlivable

6

Imagine a burst pipe flooding our apartment, a fire in the building, or severe storm damage making our unit temporarily uninhabitable. The landlord’s insurance covers the building — but where do we sleep? That’s where Lemonade‘s loss of use coverage, also called Additional Living Expenses (ALE), steps in. If a covered event makes our home unlivable, Lemonade helps pay for the cost of temporary housing above what we’d normally spend on rent.

This isn’t a minor benefit — hotel stays add up fast, especially in major cities. Having this safety net means we’re not draining our savings account just because something went wrong that was completely out of our control. Traditional insurers offer similar coverage, but the claims process is often slow and exhausting. With Lemonade’s streamlined approach, we can file a loss of use claim just as easily as any other claim, and the response time is dramatically faster than what we’d experience with a conventional provider.

See on:

Comprehensive Liability Coverage That Protects Our Financial Future

5

Accidents happen — and when they happen in our home, they can get legally complicated fast. Lemonade’s renters insurance includes personal liability coverage, which protects us if someone is injured in our apartment or if we accidentally damage someone else’s property. This isn’t just about covering a medical bill; if a guest slips and decides to sue us, Lemonade will hire a lawyer to defend us and cover the associated legal costs up to our policy’s limits.

For young renters who might not have deep savings to absorb a sudden legal judgment, this protection is invaluable. Many of us are hosting dinner parties, having friends over, or even running small home-based businesses — all situations where liability risk quietly exists. Legacy insurance companies often bury their liability terms in jargon-heavy policy documents that require a law degree to decipher. Lemonade lays everything out simply and clearly so we always know what we’re protected against and to what extent.

See on:

Personal Property Coverage That Goes Everywhere We Go

4

One of the most underrated aspects of Lemonade‘s renters insurance is the fact that our personal property coverage travels with us. That means if our laptop gets stolen from a coffee shop, our camera is damaged on a road trip, or our headphones go missing at the gym, we’re still covered — even though none of those things happened inside our apartment.

This matters enormously for our generation. We work remotely from co-working spaces. We travel. We commute with expensive gear. The idea that renters’ insurance only applies inside the four walls of our home is outdated, and Lemonade knows it. Our stuff is covered anywhere in the world, full stop. That kind of blanket protection gives us genuine peace of mind whether we’re at home in our living room or on a weekend trip across the country. No other insurer at this price point offers this level of portability with as little friction.

See on:

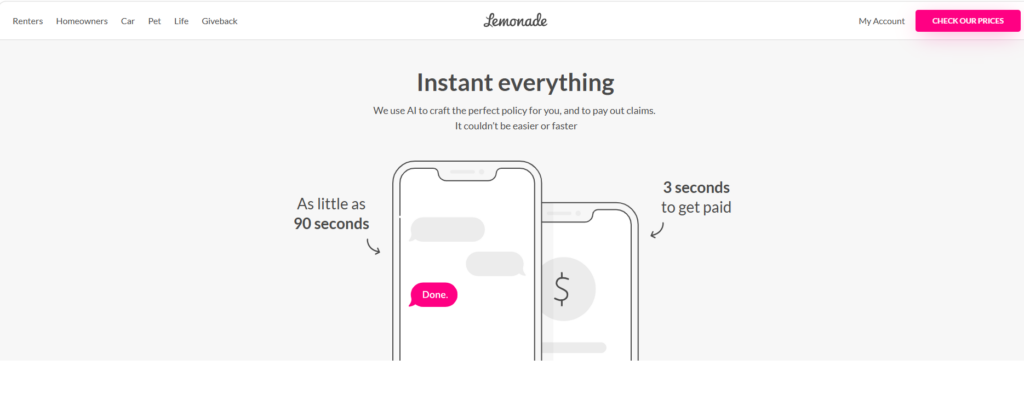

AI-Powered Claims That Can Pay Out in Seconds

3

This one genuinely blew us away the first time we heard about it. When we file a claim with Lemonade, we’re not emailing a PDF and waiting three weeks. We open the app, tap the “Claim” button, and chat with AI Jim — Lemonade’s claims-handling bot. AI Jim reviews our claim, runs it through anti-fraud checks, and in many cases, approves and processes the payment almost instantly.

As of December 2025, roughly 55% of Lemonade’s claims are fully automated, resulting in instant or near-instant payouts. There are verified customer stories of claims being settled in as little as two seconds. Traditional insurers, on the other hand, can take days or even weeks to process a claim and often require piles of documentation and multiple follow-up calls. For Gen Z and Millennials who’ve been conditioned to expect same-day delivery and real-time responses, the contrast is stark. When something goes wrong, we want it fixed fast — and Lemonade delivers exactly that.

See on:

Unbeatable Pricing That Fits a Renter’s Budget

2

Money matters — especially when we’re juggling rent, student loans, and a grocery bill that seems to go up every month. Lemonade‘s renters insurance starts at just USD 5 per month, which is genuinely one of the lowest entry points in the industry. According to internal Lemonade data from January 2026, the average cost across all customers is around USD 16 per month — and that’s for real, comprehensive coverage.

To put that in perspective, a policy from one of Lemonade’s closest competitors can cost 49% more for the same level of coverage. That’s nearly half our monthly streaming budget going straight to overpaying for insurance. With Lemonade, we get to decide exactly how much coverage we need and pick a deductible that works for our financial situation. A higher deductible lowers our monthly premium; a lower deductible means less out-of-pocket expense when we file a claim. That level of flexibility is something older, less nimble insurers simply can’t match at this price point.

See on:

Lightning-Fast Sign-Up That Takes Minutes, Not Hours

1

We’ve all been there: sitting on hold with an insurance company for 45 minutes, only to be transferred to another department. With Lemonade, that experience simply doesn’t exist. Signing up for a renters insurance policy takes just a few minutes through the Lemonade app or website, and the whole process is guided by AI Maya, Lemonade’s smart onboarding chatbot.

AI Maya asks us a handful of straightforward questions about where we live, what we own, and how much coverage we need, and then generates a personalized policy on the spot. We can get covered in the time it takes to brew a cup of coffee. No paperwork. No phone calls. No waiting. Compare this to traditional insurers that still rely on lengthy phone interviews and mailed documents, and it’s easy to see why our generation gravitates toward Lemonade. We live our lives on our phones, and Lemonade was built with exactly that in mind.

See on:

How much does Lemonade renters insurance actually cost?

Lemonade renters insurance starts at USD 5 per month, though the actual price depends on factors like where we live, how much personal property coverage we choose, and our selected deductible. As of January 2026, the average cost across Lemonade customers is around USD 16 per month. That’s significantly cheaper than the industry average, making it one of the most affordable renters insurance options available in the United States. We can get a personalized quote in minutes through the Lemonade app or website without committing to anything.

What does Lemonade renters insurance actually cover?

Lemonade’s standard renters insurance policy covers personal property against a wide range of perils, including theft, fire, smoke, vandalism, and certain types of water damage — both inside our home and anywhere in the world. It also includes personal liability coverage (protecting us if someone is injured in our home or we accidentally damage someone else’s property), medical payments to guests injured in our space, and loss of use coverage that helps pay for temporary housing if our apartment becomes uninhabitable due to a covered event. Optional add-ons are available for high-value items like jewelry, bikes, and electronics that may exceed standard sub-limits.

How does the Lemonade claims process work, and how fast is it?

Filing a claim with Lemonade is as simple as opening the app and tapping the “Claim” button. From there, AI Jim, Lemonade’s claims-handling bot, guides us through the process and reviews our claim in real time. As of late 2025, around 55% of claims are handled entirely by AI with no human intervention required, which means many claims are approved and paid out in seconds. For more complex claims, AI Jim triages the case and assigns it to a human specialist, but even in those situations, the process is dramatically faster than filing a claim with a traditional insurance company. The entire experience is designed to be stress-free, and that’s exactly what it is.

Some images on this article are copyrighted by Lemonade.